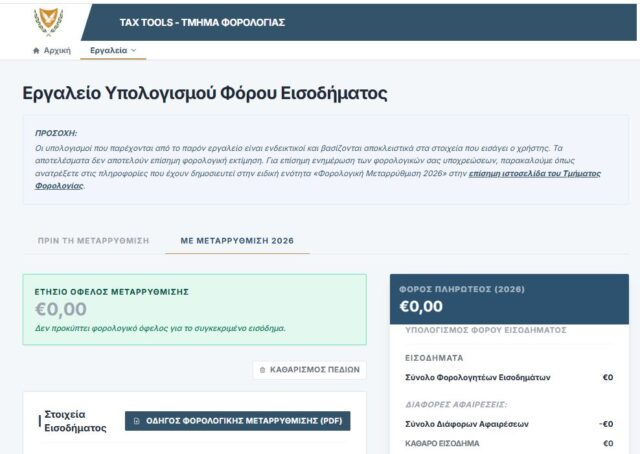

Giorgos Agapiou2026-01-20T15:13:00+03:00We inform you about the Income Tax Calculation Tool, before and after the 2026 tax reform, as posted on the Taxation Department website. You can see the tool at the link below:

Tax Tools - Τμήμα Φορολογίας

Remaining at your disposal should you have any questions.

Acute Advisory Services team

_______________________________________________________________________________________________

Σας ενημερώνουμε αναφορικά με το Εργαλείο Υπολογισμού Φόρου Εισοδήματος, πριν και μετά την φορολογική μεταρρύθμιση του 2026, όπως έχει αναρτηθεί στην ιστοσελίδα του Τμήματος Φορολογίας.

Μπορείτε να δείτε το εργαλείο στον πιο κάτω σύνδεσμο:

Tax Tools - Τμήμα Φορολογίας

Παραμένουμε στην διάθεση σας για οποιεσδήποτε απορίες.

Η ομάδα της Acute Advisory Services