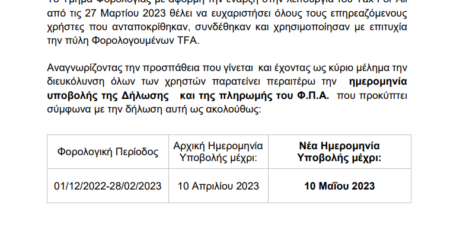

PROVISIONAL TAX

We would like to remind you that the payment deadline for the 1st provisional tax instalment for tax year 2023 is the 31st of July 2023.

Obligation for provisional tax payment

The following persons have an obligation to pay provisional tax, based on their expected annual taxable income for tax year 2023:

- Individuals with taxable income other than salaries, pensions, dividends and interest, and

- Companies with taxable income.

Payment of provisional tax

The provisional tax is calculated by applying the relevant tax rates (depending on whether the taxpayer is an individual or a company) on the expected taxable income for the year, after taking into account any overseas tax credits.

It is payable in two equal instalments, as follows:

- 1st instalment 31 July 2023

- 2nd instalment 31 December 2023

It is noted that, the final tax liability for the tax year 2023 should be settled by 1 August 2024.

If the company does not expect to have any taxable income for the year 2023, there is no requirement to pay provisional tax.

The timely payment of provisional tax can be made through the following electronic platforms:

- jccsmart.com (JCC), by clicking on Tax Department / Self Assessments / Temporary Assessment (Self-Assessment) – (0200), or

- online banking, using the unique Payment Reference Number (PRN) previously created through the Tax Portal of the Tax Department.

Payments made after the effective deadline can only be made via online banking and will be subject to interest plus a 5% penalty on the tax due.

An additional penalty of 5% may be imposed by the tax department if the tax remains unpaid two months after the statutory deadline.

10% additional tax in case of underestimation

In case the provisional taxable income declared is less than 75% of the final taxable income for the year, the taxpayer is required to pay an additional tax equal to 10% of the difference between the final tax due and the provisional tax paid.

Revised provisional tax calculation

Taxpayers can revise their provisional tax calculation (upwards/downwards) until 31 December 2023.

It is noted that for downward revisions, Forms TD.5 (for individuals) and TD.6 (for companies) should be submitted.

Remaining at your disposal should you have any questions.